We are already into the second quarter of the year, which makes this a natural moment to assess where medtech funding stands after Q1 2026. Drawing from data collected through LSI’s Compass AI platform, this analysis provides a high-level look at capital deployment, deal activity, and the broader signals shaping the current fundraising environment.

Before diving into the numbers, it is important to clarify the scope. The dataset reflects publicly disclosed rounds, spanning early angel investments through later-stage financings such as Series D and beyond. The focus remains tightly centered on medtech, software as a medical device, and diagnostics, with selective inclusion of adjacent healthtech activity when relevant signals emerge.

A Closer Look at Medtech Funding Trends

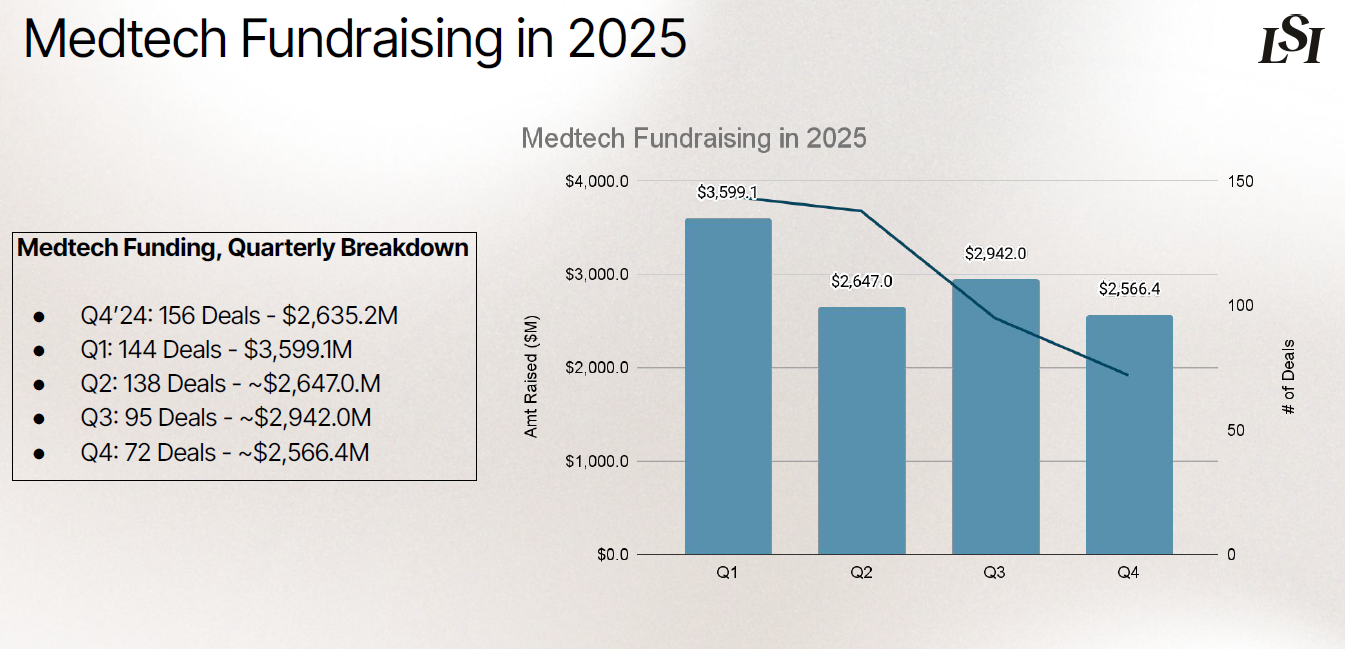

The most immediate takeaway from Q1 2026 is a clear contraction when compared to the same period last year. In Q1 2025, the industry saw $3.60 billion raised across 144 deals. In contrast, Q1 2026 recorded $2.41 billion across just 78 deals. This represents a 33.1% decline in total capital deployed and a 45.8% drop in disclosed deal volume.

Several factors help explain this shift. Macroeconomic instability continues to influence investor behavior, including geopolitical tensions that introduce broader economic uncertainty. At the same time, regulatory headwinds have slowed momentum, with ongoing disruption at the FDA contributing to longer timelines and increased caution. These pressures are layered on top of a trend toward more disciplined capital allocation, often referred to as pragmatic growth, which began in late 2024 and carried through 2025.

Despite this pullback, there are areas of resilience. M&A activity has remained active, particularly at the later stages. This has reduced the number of companies pursuing late-stage venture rounds, as acquisitions increasingly serve as an alternative exit path. It is also important to note that disclosed rounds do not capture the full picture. Based on internal estimates, total funding, including undisclosed rounds, may be approximately 1.5 times higher than reported figures. Family offices, in particular, are playing a growing role in filling early-stage gaps, though these deals are often less visible.

Looking more closely at early-stage activity, defined here as rounds of $25 million or less, these financings accounted for about 17% of total capital in Q1 2026. This is slightly down from 18.4% in Q1 2025, suggesting that early innovation continues to attract capital, but at a somewhat reduced pace.

Another notable shift is the decline in mega rounds. In Q1 2025, there were 12 rounds exceeding $100 million. That number dropped to just 6 in Q1 2026. Total capital raised in these large rounds fell from $1.48 billion to $735.0 million, representing the most significant contributor to the overall decrease in funding.

When viewed in a broader context, however, the current environment appears less dramatic. The surge in late 2024 and early 2025 was driven in part by optimism around macroeconomic conditions that ultimately did not materialize. The current slowdown reflects a normalization rather than a collapse.

The Role of LSI Alumni in Q1 2026

Within this environment, LSI Alumni companies continue to represent a meaningful share of activity. There are approximately 2,200 companies in the LSI Alumni ecosystem, and in Q1 2026, LSI Alumni collectively raised $1.2 billion. This accounts for 49.5% of all tracked capital during the quarter.

The impact is even more pronounced at the early stage, where LSI Alumni companies were responsible for roughly 70% of capital raised. This highlights the continued importance of connectivity between investors and emerging companies, particularly during periods of tighter capital availability.

Sector Momentum and Capital Allocation

Certain segments continue to stand out in terms of investor interest. Neuro and brain tech remain highly active, driven in part by demand for solutions addressing Alzheimer’s disease. The pipeline for disease-modifying therapies is driving increased need for early diagnostics and intervention.

Cardiovascular and endovascular interventions also continue to attract consistent capital, with particular focus on valves for structural heart disease, clot removal technologies across peripheral and neurovascular applications, and heart failure management. In parallel, surgical robotics remains a major area of investment, as both established players and new entrants push forward with next-generation systems.

These themes are not new but rather represent a continuation of trends that defined 2025, reinforcing the idea that capital is concentrating around areas with clear clinical need and strong market potential.

Stabilization Beneath the Surface

So, is this a downturn or part of a larger cycle? While Q1 2026 reflects a slowdown, a wider lens suggests a more stable picture. Capital deployment has remained relatively consistent over multiple quarters, even as external challenges have intensified.

At the same time, new investment funds continue to close, and new firms are entering the space. Conversations with investors indicate ongoing interest in the sector, even if deployment is more selective.

The broader takeaway is that medtech funding is adjusting rather than retreating. Innovation in healthcare remains essential, and the demand for new solutions continues to drive long-term interest. While the pace may fluctuate, the foundation of the industry remains strong, supported by a steady pipeline of companies working to address some of the most pressing challenges in medicine.

© 2026 Life Science Intelligence, Inc., All Rights Reserved. | Privacy Policy | Your Privacy Choices | Delete my Data